Working holiday makers (WHMs) are temporary visitors to Australia who hold a Working Holiday visa (subclass 417) or Work and Holiday visa (subclass 462), learn more from the ATO

A working holiday maker can be an "Australian Resident" for tax purposes if the taxpayer meet the criteria required by ATO. Link from ATO

When Salary or wage amount is presented with working holiday visa then A4 WHM Net income must also be presented. Calculation of tax on taxable income depends on this.

Switch-on "Adjustments" icon via 4 little square

Click "Income" tab and select "PAYG", then press "Add Worksheet" -

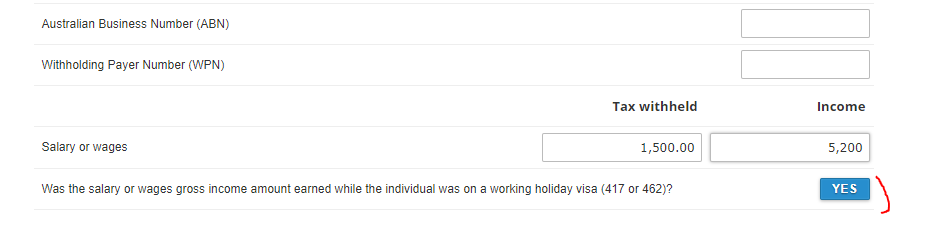

On Salary or wages worksheet user must select True for Working holiday makers question.

When Salary or wage amount is presented with working holiday visa then A4 WHM Net income must also be presented via "Adjustments" tab. Calculation of tax on taxable income depends on this. Learn more

Go to "Adjustments" Tab

Note that any of the following fields must be filled if there is an amount in A4 Working holiday maker net income.

- A salary or wage associated with working holiday maker income;

- Share of net income from trusts less capital gains, foreign income and franked distributions;

- Net non-Primary Production income/loss;

- Net small business income.

How Tax Estimate is calculated for part-year resident Working Holiday Maker?

If the resident taxpayer is a working holiday maker at any time during the year of income:

(a) Count the taxpayer’s working holiday taxable income for the year of income as the first parts (starting from $0) of the taxpayer’s ordinary taxable income for the purposes of the table in clause 1; Income Tax Rates Amendment (Working Holiday Maker Reform) Act 2016, Clause 4.

A working holiday maker earned $20,000 in July and August 2019. In September 2019 she became a resident. Then she earned $70,000 in the rest of the financial year.

The tax payable calculated as below:

| Taxable Income | Tax Rate | Tax | Comment |

| $1- $20, 000 | 15% | $3,000 | ato.gov.au - Working holiday makers |

| $20.001 - $37,000 | 19% | $3,230 | 19% applied since the first part of the income exceed the tax free threshold $18200 |

| $37,001 - $90,000 | 32.50% | $17,225 | Marginal rate |

| Total Tax Payable | $23,455 |

Note: If the you find LodgeiT calculation is different, after about two weeks ATO will send the Notice of assessment with correct calculation which will also be visible in LodgeiT.

Note: If expecting a "Refund", make sure to delete "Australian Residency Start and End Dates",

and "Number of Months eligible for part year tax free threshold" via "Adjustment" tab