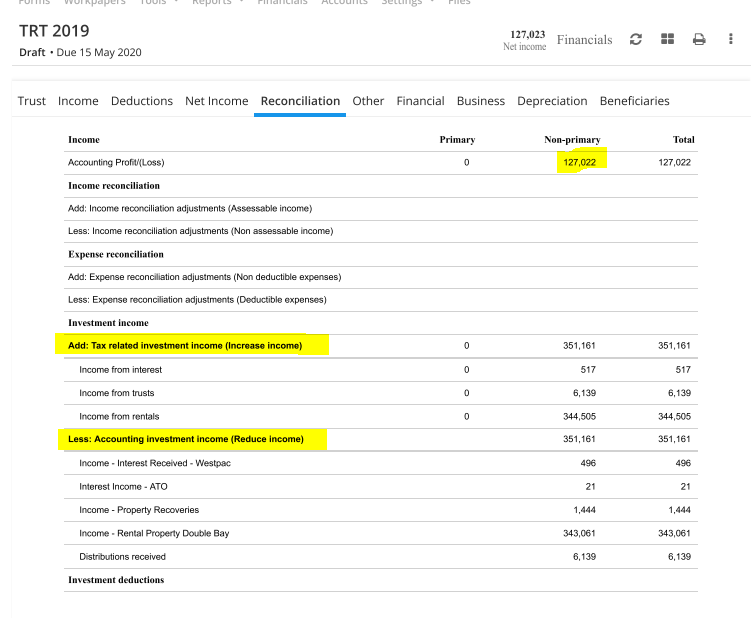

The reconciliation section of a tax return allows the accounting income to be reconciled to the taxable income. The reason for this is that certain income items may not be assessable or the amounts may differ. Similarly, with expenses, some accounting amounts may not be deductible or amounts may differ.

To explain the Reconciliation -

It is quite common that accounting and tax facts may not be the same, particularly in respect to investment income. LodgeiT Reconciliation demonstrates how tax facts are arrived at from accounting facts. In the example below, the noted accounting facts are backed out and the tax facts are included.

Example 1:

Example 2:

Adjust/add the item via "Income" tab -

It will now show under "Reconciliation" tab

For SBE, click here - Simplified Depreciation Rules "Depreciation Expenses on Accounts"

Related Article:

Trust Income Earned by a Trust